Entering retirement should be exciting… but not for reasons related to your investment portfolio! The financial transition into retirement definitely takes planning, but large changes to your portfolio are rarely warranted. As we often say, your portfolio is like a bar of soap; the more you touch it, the smaller it gets.

During the accumulation phase, every market correction is a buying opportunity. In retirement, however, corrections can bring anxiety, as you may be forced to take money out during market dips. Thus, finding the right balance between growth and stability in your portfolio is both a mathematical and psychological endeavor.

Navigating the Long Haul

It might be helpful to think of retirement as a journey across a large body of water. You will need a boat sizeable enough to tackle challenging waves, but enough speed is required to eventually reach your destination. In terms of investing, the size of your boat refers to your asset allocation…or the mix between riskier and safer assets. A higher percentage of stable assets (i.e. a larger boat) will ensure that you survive large market corrections.

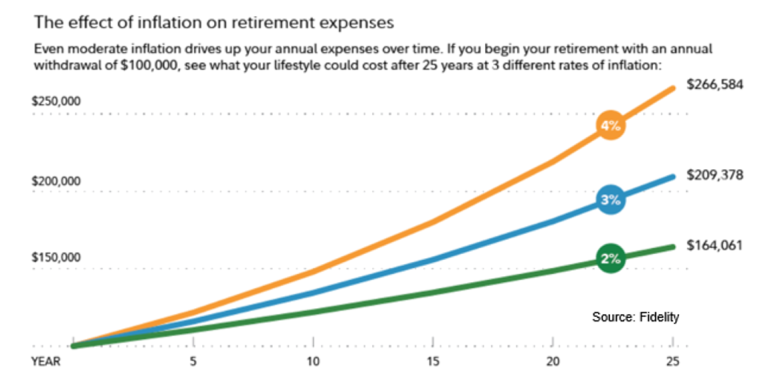

But beware! There is an often unseen danger lurking deep in the water that can take out big ships. That danger is inflation. Your portfolio might generate enough income to live on at today’s prices, but can it meet future years’ needs? The chart below highlights how $100,000 of expenses can multiply over time. At 3% inflation, you will need more than double the income 25 years later. A portfolio consisting mainly of safe assets will not protect you against this risk. The portfolio that is least risky in the long run may ironically have more short-term risk.

Finding the Balance

Selecting the right asset allocation is one of the biggest pieces to your retirement puzzle. This assumes you are properly diversified and don’t mess up the long-term plan with short-term emotional decisions (remember the bar of soap).

In addition to income requirements and risk tolerance, other factors that could impact your asset allocation decision include:

- Investment Time Horizon: Are you retiring at age 70 or age 50?

- Level of Liquidity Reserves: Can you turn off distributions during a market downturn?

- Potential Inheritance: Do you expect to receive other resources?

- Downsizing of Real Estate: Selling a large house could unlock investable assets.

- Flexibility to Adjust Spending: Can you engage in part-time work if necessary?

- Large Expected Outlays: Do you need to purchase a car or put a new roof on the house?

- Support of Others: Are your children financially independent, or could they need help?

- Legacy: Is your goal to leave a large balance to heirs or charitable organizations?

- Healthcare Needs: While tough to predict, does your plan have a margin of error?

Your advisor has the modeling tools to assess these “what-if” scenarios and to help you arrive at the allocation that provides financial and emotional comfort. Of course, all plans need periodic reviews and potential tweaks, and asset allocation is just one component of the financial planning landscape.

Happy sailing! I hope you stay mostly dry.