As advisors who help Midwestern families pursue thoughtful financial strategies, we’re always on the lookout for new planning opportunities. Especially when those opportunities align with your long-term goals. One of the most talked-about savings tools of 2026 is the new “Trump Account” (officially known as a Section 530A account). These are unique, tax-advantaged investment accounts for children created under federal law.

In this blog, we’ll explain what Trump Accounts are, their potential benefits and limitations, and how they compare to current saving vehicles like UTMA/UGMA custodial accounts and 529 education savings plans. We will also provide a brief outline of how to set up the account and obtain the funding for children born between 1/1/2025 and 12/31/2028.

What Is a Trump Account?

The “Trump Account” is a new tax-favored savings and investment account established by the federal government for the exclusive benefit of a child under age 18. It functions similarly to a traditional IRA but is tailored specifically for children.

Key Details:

- Initial Funding: Children who are U.S. citizens born between January 1, 2025, and December 31, 2028 are eligible for a one-time $1,000 contribution from the U.S. Treasury.

- Contributions: Starting July 4, 2026, parents, family members, employers, and even charities can contribute up to $5,000 per year (not counting the government seed contribution). These contributions are made with after-tax dollars and are not tax-deductible to an individual making the contribution.

- Investment Requirements: Funds must be invested in low-cost broad U.S. equity index mutual funds or ETFs.

- Age of Maturity: Until the beneficiary turns 18, withdrawals are generally restricted. After that, the account transitions to traditional IRA rules, and the individual controls the funds.

In essence, Trump Accounts are a tax-deferred IRA-style investment account for kids, different from an education savings vehicle or a regular custodial account.

Benefits of the New Accounts

- Initial Funding: Eligible children automatically receive $1,000 from the Treasury. This functions as a head start that you don’t have to fund out of pocket.

- Tax-Deferred Growth: Earnings grow tax-deferred, meaning you won’t owe tax on dividends or gains while the money is invested. This is very similar to traditional retirement accounts.

- Family & Employer Contributions: Multiple parties can contribute up to the $5,000 annual cap, including employers (up to $2,500) and nonprofit entities.

- Low Fees & Simple Investments: By law, investment options are limited to broad market index funds with a 0.10% fee cap, keeping costs low.

- Flexibility After Age 18: Once the child turns 18, the account generally follows traditional IRA distribution rules. Ultimately, meaning the funds could be used for education, a first home, or retirement.

Cons of the New Accounts

- Limited Access Before Age 18: You generally cannot use the money for any purpose before age 18. This makes the Trump Accounts less flexible for early education or other younger-age goals.

- Taxation After Age 18: Withdrawals once the account operates like an IRA are subject to ordinary income tax, which can be less favorable than a taxable investment held by parents in a UTMA/UGMA account.

- Less Flexibility in Investment Choice: Unlike a UTMA or 529 plan, the new accounts restrict investments to broad U.S. equity indexes. As of now, there are no bonds, cash alternatives, or individual stock picks. The lack of diversification is a limiting factor.

- Financial Aid Impact: Because the account is in the child’s name, balances may count in financial aid formulas, potentially reducing aid eligibility. 529 plans are counted as parents’ assets, so the impact is not as significant when applying for financial aid.

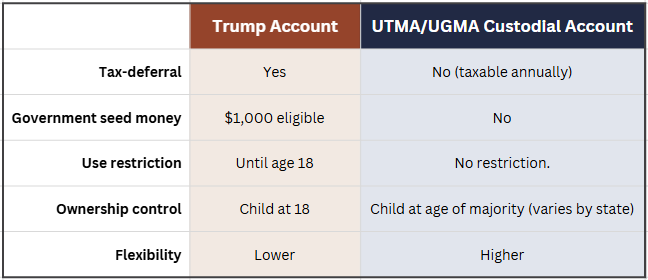

Trump Accounts vs. UTMA/UGMA Accounts

UTMA/UGMA accounts let parents gift assets to a minor, but once the child hits the age of majority (often 18 or 21), they legally own the funds and can use them for anything. Earnings are taxed yearly under the kiddie tax rules, which can be favorable for smaller investment gains.

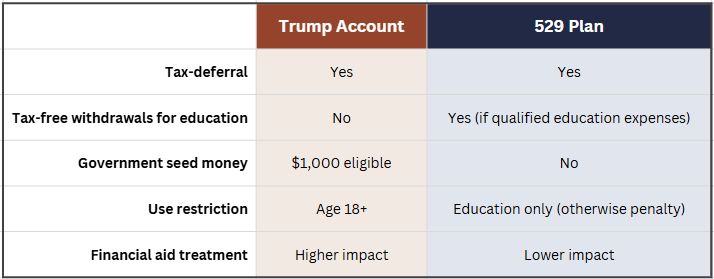

Trump Accounts vs. 529 Education Savings

529 plans remain one of the most efficient vehicles for education savings because earnings are tax-free when used for qualified education expenses, and the list of eligible expenses has been broadened after recent updates. Examples of the expansion of those expenses include the K-12 limit increases, additional expense eligibility, and vocational training.

Trump Accounts don’t offer tax-free withdrawals for education. Earnings are taxed upon distribution, but they do offer flexibility for broader future goals and that early government contribution.

Claiming a Trump Account for Your Children

To establish a Trump Account (and claim the $1,000 Treasury seed for eligible children), you must file IRS Form 4547 in one of two ways:

- With your 2025 tax return (filed in 2026) by attaching Form 4547 to elect the account and request the pilot contribution.

- Online, once the IRS/TrumpAccounts.gov portal opens. This is expected in mid-2026 and is accomplished by submitting the equivalent election.

After the IRS processes the election, the Treasury sends activation instructions, and you complete setup with the designated trustee before contributions begin on July 4, 2026.

According to the IRS, an authorized individual (usually a parent, legal guardian, adult sibling, or grandparent) must make the election on the child’s behalf.

Major Highlights & Takeaways

Trump Accounts offer an intriguing new way to jump-start long-term savings for children by combining tax-deferral, government seed money, and IRA-style investing. For some families, especially those focused on retirement or long-term wealth accumulation for their children, this could be a valuable complement to existing strategies.

However, if education savings, early access, or flexibility are your priorities, 529 plans and UTMA/UGMA custodial accounts may still better achieve those goals as part of your planning.

As always, integrating any new account type into a family’s financial plan should be done thoughtfully and in the context of broader goals, from college funding to retirement legacy planning.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.